(Post 219 of 263)

I’m coming to a year of being a client of BBVA. There have been a couple of small hiccups, but, overall, I have been thrilled with their service. When I opened the account in October, they said that I would be able to get a credit card within six months. They kept that promise in February. At that time, my limit was pretty low and they said I would be able to increase it within a year. That happened last week!

I had a little popup on the phone app that said I was eligible for a limit increase. I thought that if I pressed accept I would start a process of having to go in to my branch to sign paperwork that would be preapproved at the branch level but have to be escalated up to CDMX for final approval, same as with my credit card. Nope, the increase went through automatically!

Increasing the limit on the card was getting important so that I could start taking advantage of “months without interest” promotions that would allow me to continue to build up my credit limit here in the hope of getting a car loan and/or mortgage in the future. The initial limit was just enough for my monthly expenditures. If I took a months without interest promotion, that would tie up my balance, rendering the card useless until it was paid off. Sure, I could pay with my debit card, but I get points with my credit card. It’s not a ton of money, I’ve been getting about $500 a month, but I haven’t had to pay for coffee in months and my last regular visit to the dentist was free. So not using the card would be like throwing away free money!

Getting this increase coincided with the new iPhone having been released and I am desperately due for a new phone. You can’t get by here efficiently without a working smartphone — life effectively runs off them. My XR constantly overheats and randomly shuts down, which has caused me issues with Uber. I’ve never had the top line current model of a smart phone and have had two lower-end iPhones that were not great. Time to get current. iShop offered me a rebate equivalent to current market value (!) for my XR if I exchanged it for a new phone, which dropped the price of the phone I want by nearly 20%! They also offer up to 20 interest-free payments on my BBVA card and, get this, the new card limit increase is almost exactly the price of the phone. So I can finance the phone at no cost and still have the same balance on my card as before for daily use and, of course, I’ll keep freeing up balance every month as I make my payments. I also have the option of clearing the balance without penalty if I want. I’m not sure if I get points for a months without interest purchase, though that would rather be like getting your cake and eating too. I’ll know once I buy the phone as that would significantly increase my points balance.

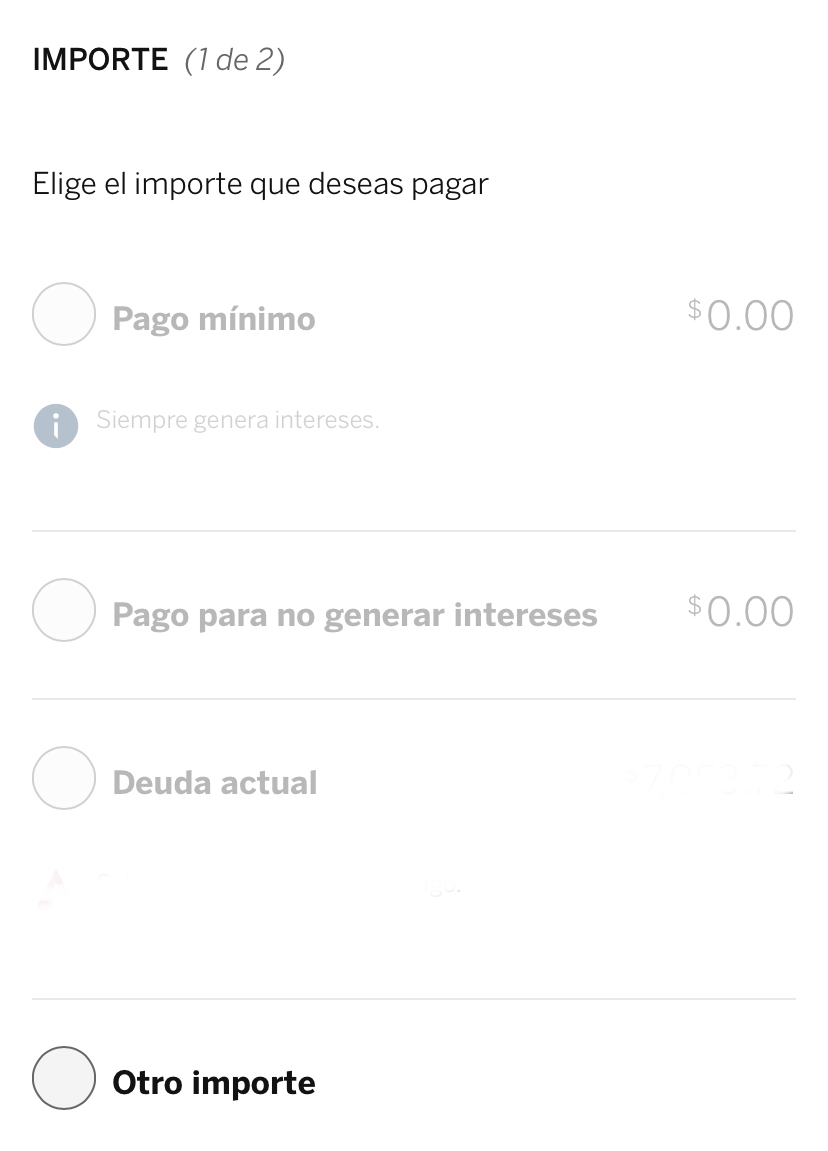

I did one of the months without interest promotions with Home Depot to see how it works and it’s a bit confusing, at least in the app. In my account transactions, I see the initial amount charged to my card on the day of but then they also have a debit for the first payment. It feels like I’m paying twice, but the math looks correct on the statement. I like that it’s very easy for me to track on my end because when you pay your card, BBVA spells out your minimum payment (clarifying that you will pay interest), the amount to pay to avoid interest, and then what you need to pay to clear the balance. You can also make an “other” payment. I do that sometimes mid month to free up some balance. Last month, doing that did not affect my Home Depot promo — they applied that extra payment to other purchases.

I appreciate BBVA helping me feel like I actually live here so that I can keep cutting my ties to Canada. Having a credit card here is really make my finances easier to manage because I have so many fewer cross-border transactions. I pretty much only use my Canadian credit card for business purchases now.